If the Fiduciary Rule is Killed, Will Any Advisors act in Your Best Interest?

Here’s why wealthy investors don’t lose money in the stock market

March 7, 2018

Socially Responsible Investing: This Isn’t A Fad

November 7, 2018

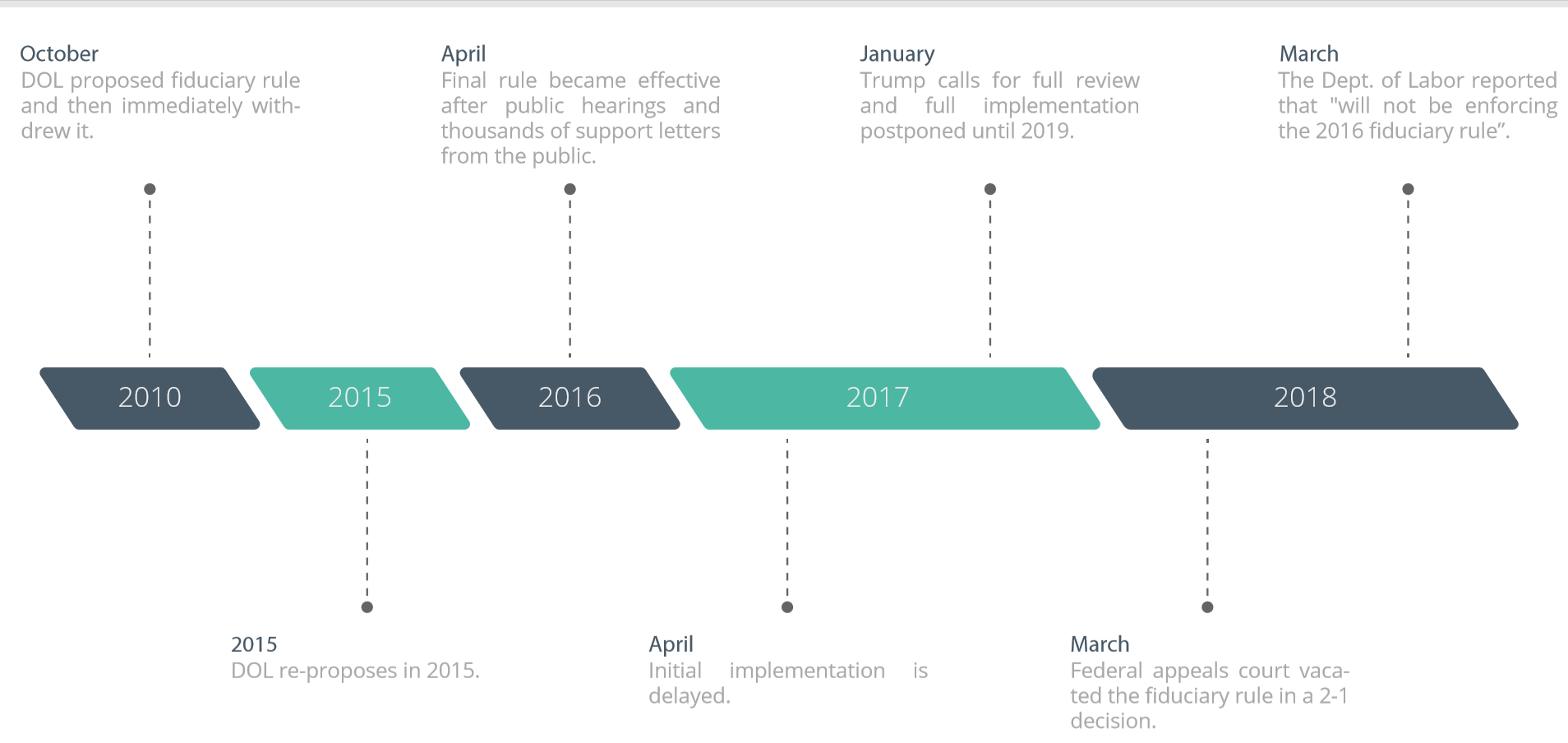

The whole idea behind the Department of Labor’s Fiduciary Rule was to protect consumers from the blatant conflicts of interest that are standard operating practice in the brokerage business. The rule wasn’t perfect, but it was going to require all financial advisors to make their clients’ financial well-being their top-most priority. That sounds pretty basic. If you’re going to pay a professional advisor for his financial and investment advice, shouldn’t he have a legal or fiduciary responsibility to act in your best interest? The fiduciary rule was supposed to ensure that would be the case, and it was expected to go into full effect this year, but rules are meant to be broken.

Portions of the fiduciary rule were implemented, but the final piece that hasn’t been enacted yet would require brokers to reveal all conflicts of interest related to their investment recommendations in which the broker receives commissions or kickbacks. In other words, this is a rule that mandates full transparency for all those hidden costs and/or motivations tied to those investment recommendations. The current administration wants to leave the industry as is, and is well on its way to rolling back the rule that the Obama administration tried to push forward and so far has managed to delay implementation of the final piece. Then last month, a federal appeals court voted to abandon the fiduciary rule altogether, stating that the Department of Labor had overstepped its boundaries.

So where does this leave you?

Fortunately, the fiduciary rule making headlines is enough of a red flag to alert consumers who care about the quality of the financial advice they’re paying for. So if the fiduciary rule is going away, does it mean that high-quality, fiduciary-level advice is also no longer accessible? Thankfully, the answer is no, not at all. All you need is to understand that advisors play by two different sets of rules and that one set demands a much higher standard than the other. You, the consumer, are holding all the cards and can choose to work only with advisors who bother to practice at the higher fiduciary standard.

You do have a choice

Brokers and insurance agents are salespeople and they’re paid to sell transactions on behalf of their firms. They do not work for you. They work in their firms’ best interests which begs the question: who’s to say a salesperson’s advice is subpar compared to a fiduciary advisor? financial advice you get from brokers and insurance agents is subpar? Believe it or not, it’s the brokers and insurance agents themselves. They are lobbying hard to be allowed to stick to the lowest possible standard of responsibility to you, the client. Independent financial advisors who are registered with the state or SEC can’t hide behind their firms. Independent advisors have a different business model. Those advisors must legally adhere to the higher ‘best interest’ standard. The fact is, you can choose to engage with any number of fiduciary advisors who work only and directly for you, and who are willing to sign an oath to that effect. A competent fiduciary financial advisor doesn’t sell investments. That doesn’t guarantee competency, but he is much more likely to have the education and experience to provide detailed financial planning and cash flow analysis. Most brokers cannot offer this level of analysis because they get paid to sell, not to plan. At least now you know there is a higher fiduciary standard of conduct and it’s not going away, but only about 10% of financial advisors follow the fiduciary standard. This is why you have to choose wisely.

Your own financial strategy

If you’re about to step over the starting line into retirement, a thorough look at your cash flow and stress-testing the amount you plan to withdraw from your savings each year in retirement are critically important. It’s about developing a plan that helps prevent from running out of money in retirement. Once you know where you stand, then you can you intelligently execute on your investment strategy. Brokers and insurance agents often skip over the critical planning details and dive right into a strong sales pitch about how the products they sell will supposedly rise when the markets are up, and then protect you from losses when it falls. If you didn’t know better, you might invest all of your savings out of fear of missing out. What most people find out much later is that these products, like variable annuities, come with many complicated strings attached and offer much lower returns with much higher costs and punitive early withdrawal fees.

You don’t need anyone to make a rule to protect yourself. Just make your own fiduciary rule: don’t hire an investment advisor who cannot sign a fiduciary oath.

1 Comment

This was one of my greatest fears, so I’m glad to hear this! Now if only I could figure out where to find one locally. It’s not like you can look in the yellow pages anymore…